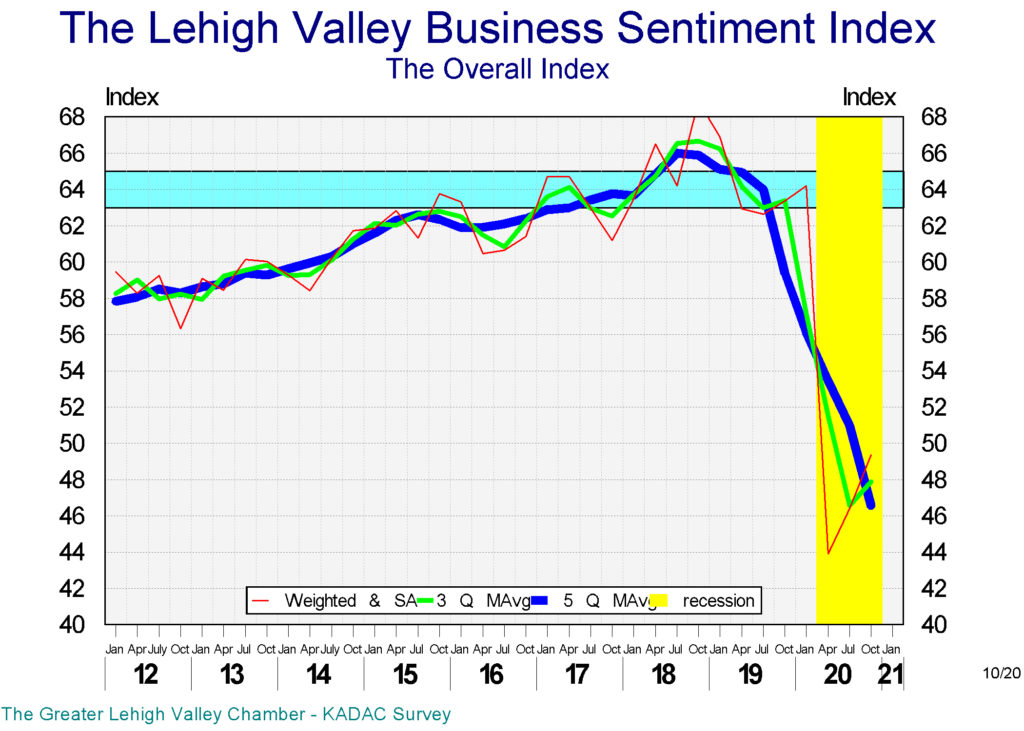

Lehigh Valley business sentiment index rose 6.4% in October

The Lehigh Valley’s business sentiment index the BSI made another small recovery in October, rising by 6.4%, similar to its 5.7% increase in July, after its historical 31.6% fall in April. Even after two increases, the October index rose to only 49.4, well below its January level of 64.2. And still below its average level during the Great Recession. The index’s improvement is underwhelming, too small, and reeks of a lack of enthusiasm from the Valley’s businesses participating in the survey.

Our October survey of Valley businesses was done before the release of the advanced estimate for the US economic growth, which shows a 33.1% increase in the 3rd quarter’s GDP, after an unexpected 31.4% drop in the 2nd quarter as the results of the Covid-19 and all the shutdowns. Despite the large percentage gain, since it was from a smaller base, the GDP rose to only 91.3% of its previous level, leaving us $670 billion short of its last year’s level.

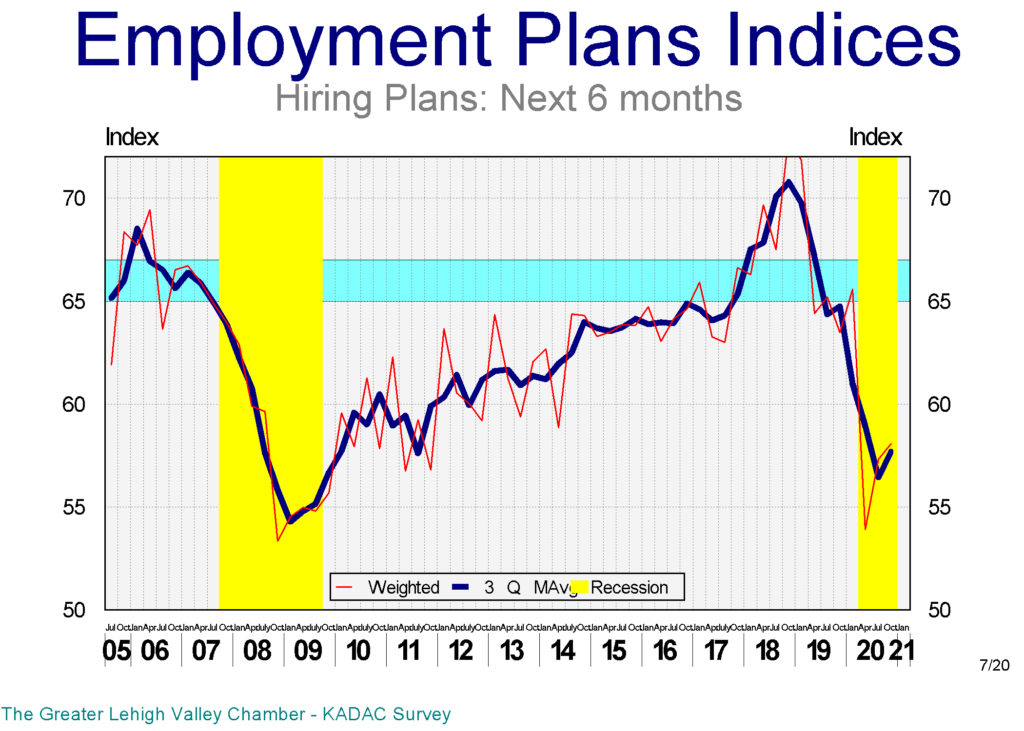

In our Lehigh Valley model, the largest gain was for the new hires’ index in the last 6 months, which rose by 10.4% since July. Unfortunately, the index is still 26.6% below its last year’s level, even with that increase. Plans for future hiring did not show any measurable changes since July. Its index is still 8.5% below its last year’s level, and worse, the momentum for both hiring indices is negative and lower than any time even during the Great Recession.

The percent of local companies that reported net layoffs were around 5% during 2018 & 19, while the percentage of those with net hiring hovered close to 30%. These ratios have changed dramatically; in October, 27.1% of the participants in our survey had net layoffs, while only 15.5% of them reported net hiring. To simplify it, layoffs have increased by 5 fold, while hiring dropped in half.

As was expected, accommodation-food & leisure sector had the largest layoffs by far over the last 6 months. That dubious distinction still follows the sector as it also has led in layoff plans for the next 6 months.

Retail and other services sectors had the largest net hiring in the last 6 months, while manufacturing is the lead in hiring plans for the next 6 months.

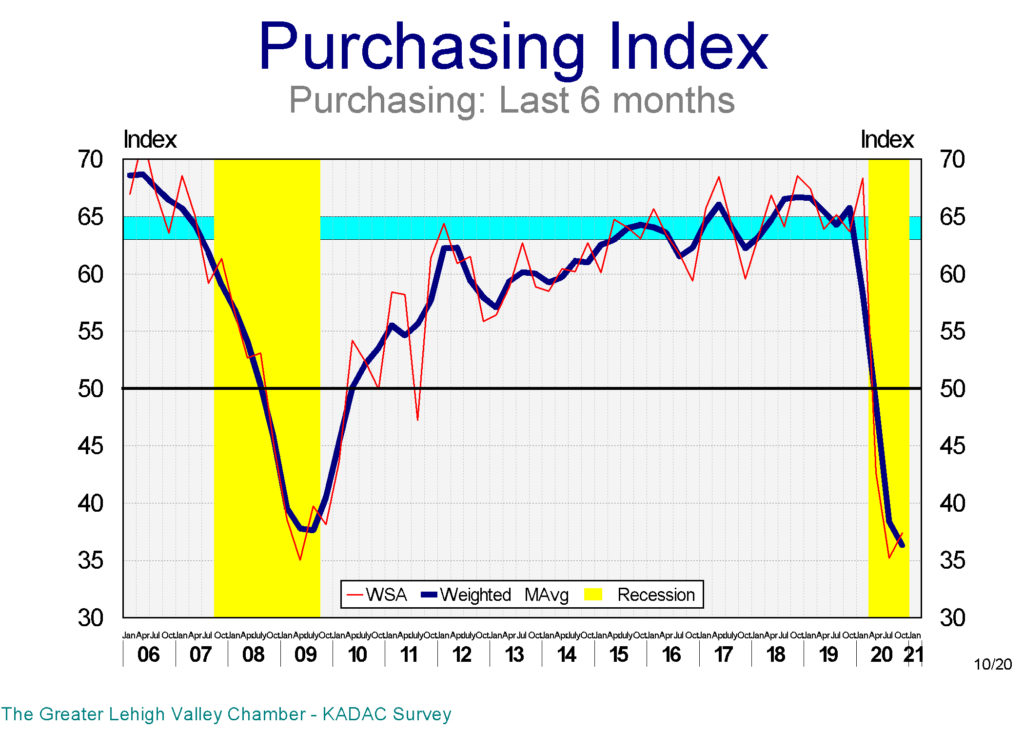

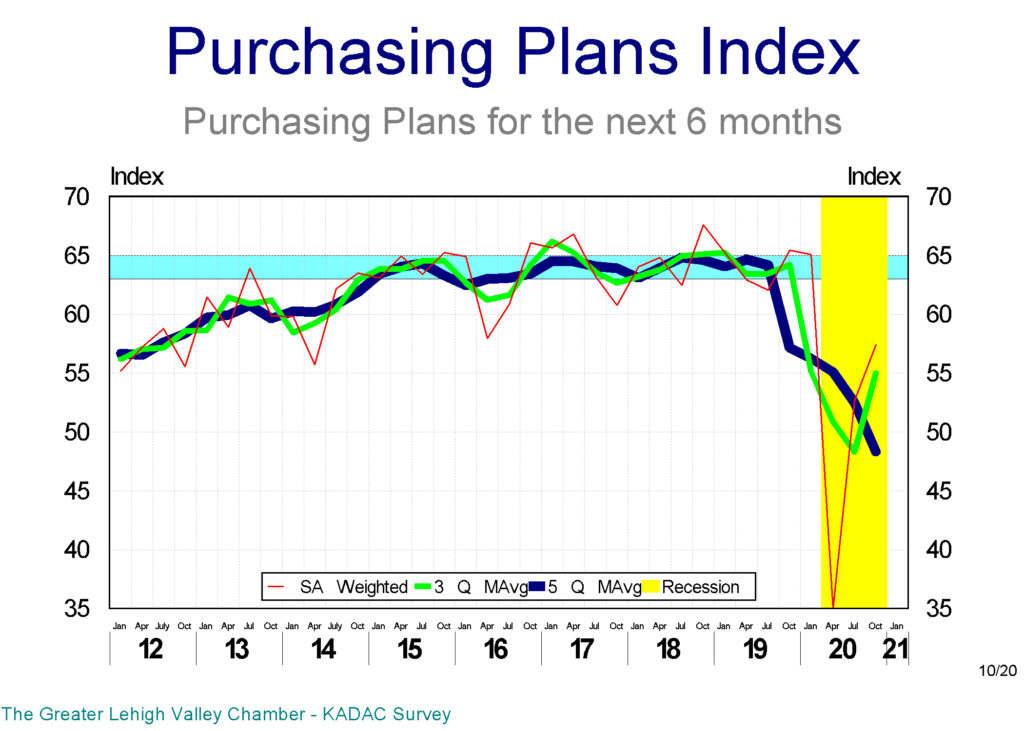

Purchasing plans indices also rose in October; actual purchases recorded a 6.2% increase while plans for future purchases rose by 9.0%. However, to put these in context, actual purchases are still 41.3% below where they were last year despite the October increase. Plans for future purchases is in better shape and is only 12.3% below its last year’s level.

Accommodation-food & leisure sector also had the largest cutbacks in purchasing over the last 6 months. And they also lead the plans for cutbacks among other sectors over the next 6 months. The manufacturing sector leads the purchasing plans for the next 6 months.

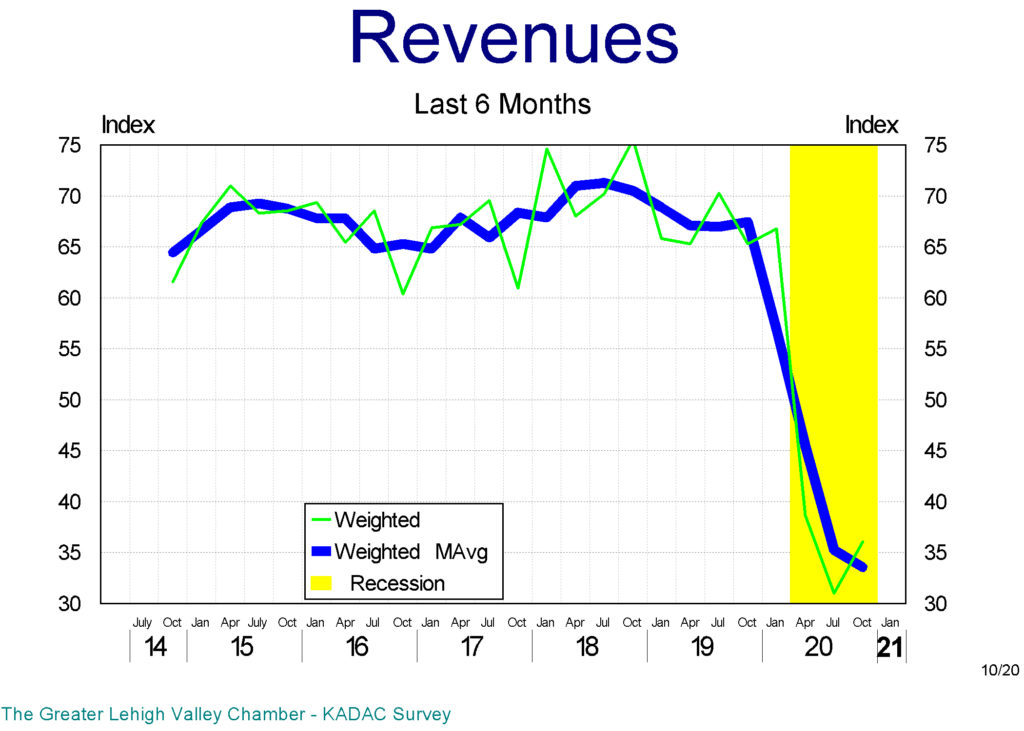

It was a different story when it came to revenues; not everybody was in the same boat. While Real Estate companies reported very large increases in their revenues over the last 6 months, other sectors reported significant losses. The only exception was the professional and scientific sector, which reported a small increase in their revenues.

Healthcare leads the expected rise in revenues over the next 6 months, while accommodation-food & leisure sector still expects large drops in their revenues.

The economy reclaimed a good 91% of its losses during the 2nd quarter, however, it is still well below its last year’s level. The most common question is; was the 3rd quarter growth the start of a V-shaped recovery or the end of the first up-tick inside a W-shaped recovery. Which translates to, is this the start of continuous recovery, or are we in for a second drop in the GDP.

Our local business survey clearly shows a heightened level of concern with the future of the economy. We did not observe any of the common signs when enthusiasm about the future counters fears of the present and usually results in sustained growth, something that was part and parcel of all previous recoveries.

This time around, businesses are not setting-up for recovery, it looks like they are more concerned with further risk reduction.