Oil market glut is continuing to expand, surprisingly, so is the price of oil

Forecasting oil prices with any reasonable accuracy appears to be beyond the scientific abilities of many economists. At times it appears that this task is more in the realm of art rather than the science of forecasting.

The basic methodology of any price analysis is to brake the market into its primary components, supply and demand. As I use to tell my students, economics is an easy subject.

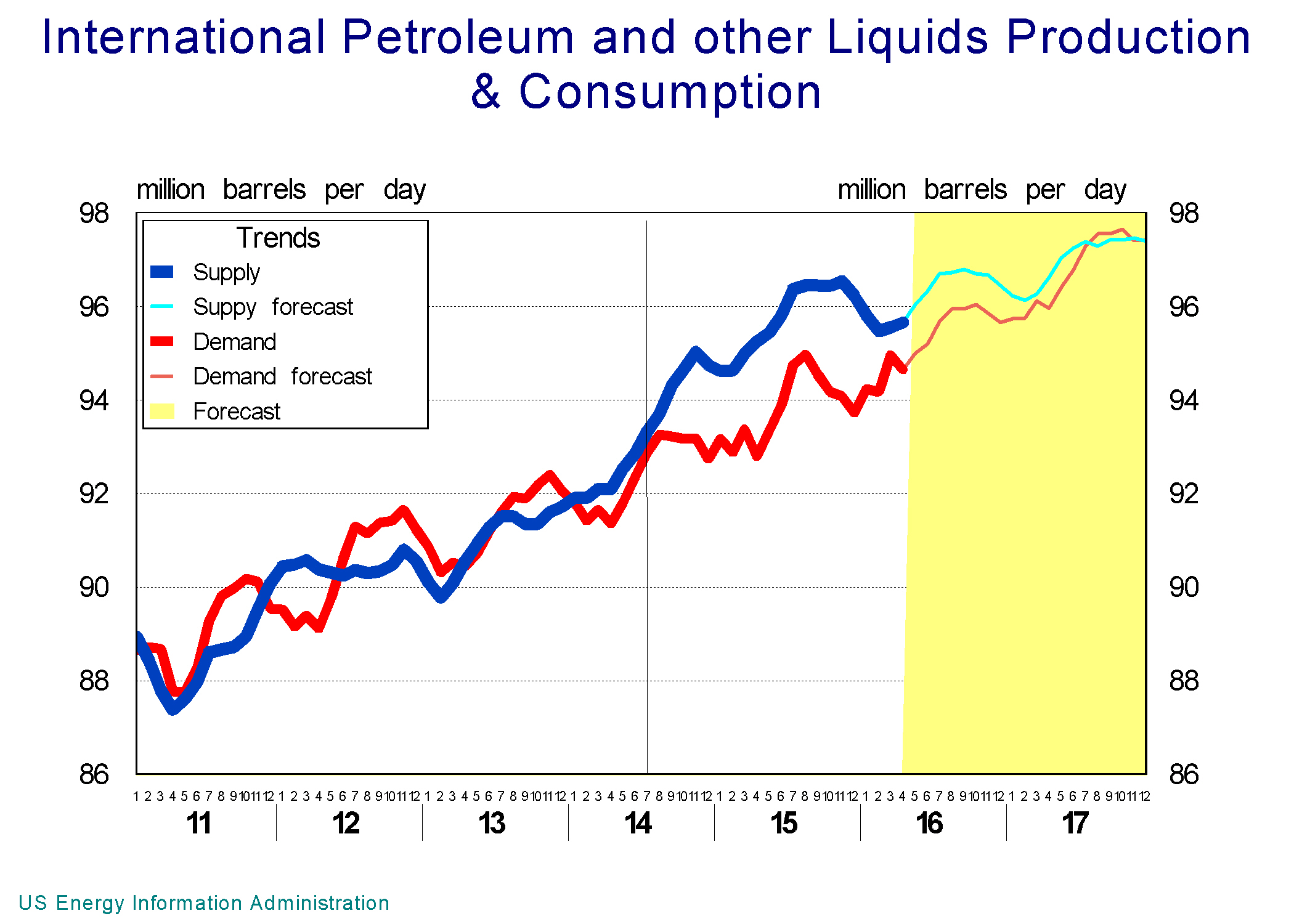

Starting with supply of oil; during the first half of 2014 and before oil prices crashed, global supply of oil was hovering at around 92 million barrels per day, about 0.6 million barrels of daily over supply. Despite of that oil prices rose by about 5% during the same period. During the second half of 2014, oil production increased by more than 2 million barrels a day, increasing the daily surplus to 1.1 million barrels. This resulted in a sizeable increase in oil inventories accompanied with a 44% drop in the price of oil.

Cushing Oklahoma is a vital transshipment and storage facility in the US, its storage reserves rose by 45% during the second half of 2014.

Thus far the basic tenets of economics have worked, as supply increased faster than demand, prices dropped and inventories rose. Didn’t I say economics is easy.

Well, here is where we have to make some minor adjustments to the simple pricing model to explain why a 2% increase in production has caused a 44% drop in prices.

In reality the pricing models are more complicated than what I initially alluded to, we have to allow for a number of variables, from the simple ones like supply and demand, to some more complex ones like expectations of the future. And then of course there is an array of other variables, like the asymmetric production cost variables, that has to be considered. Well I guess some of my students may have had a point, economics is not all that easy.

As of the second week of May, oil prices have shown an increase of 31% for the year, despite the fact that during the same period there was an average of 1.4 million barrels of daily surplus added to the market, further inflating oil storage inventories.

Cushing reserves are at more than triple the level they were when oil prices started to drop in 2014, total oil supplies have risen to an estimated 96 million barrels per day which is projected to create 1 million barrels of daily surplus for the balance of the year according to the US Energy Information Administration (EIA). However, and in the same publication EIA also forecasts a significant 10% increase in price of oil by end of the year.

Interestingly enough, as of this writing, the price of oil has already surpassed the EIA’s forecast despite the historically high and continually expanding sea of oil storage inventories.